Embracing a digital operating model: a call to action for banks (3)

Find them on LinkedIn: David Cox & Annette Harris

Part 1: broken experiences | Part 2: engines of innovation| Part 3: out with the old

Part 3 of 3: out with the old

This is the final post of our three-part series. In our first post, we discussed the importance of developing a customer-centric operating model. In the second, we looked at the seismic shifts underway in the financial services industry and the need to move quickly to incorporate a new data architecture and an analytics framework for a new digital operating model. Now we will turn our focus to how banks can make it happen.

The modernization trap

One of our customers recently had a stream of projects to improve their business. But they freely admitted they were struggling to do all of them with their available resources and bandwidth. Then they shared with us a study from another firm they had commissioned a few years ago listing the same projects. They had plans to move to the cloud one day when all those projects were complete.

It quickly became apparent the bank was trying to modernize its environment. But they weren’t transforming it. They were doing all the things other banks do but they weren’t leading the market’s transformation. In fact, by the time they succeeded in modernizing their environment, they were more than likely to be overwhelmed by the disruption now prevalent in the industry.

It is not enough today to have cloud capabilities. The operating model needs to be cloud-based because such a model dramatically increases speed, agility, and efficiency. Being native to the cloud is a different way of working: it’s agile; it’s flexible; and there’s enhanced speed to market.

In with the new

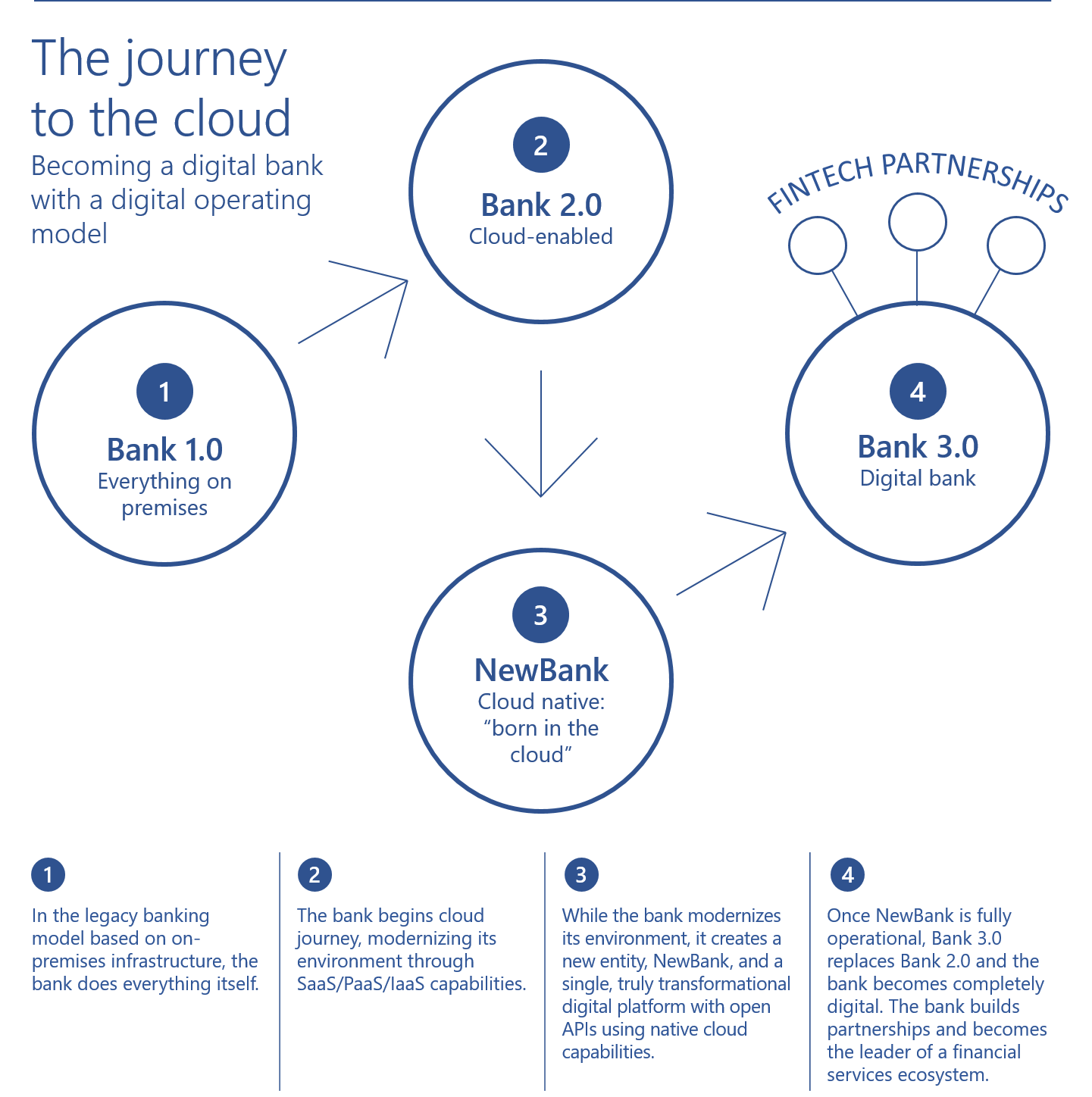

But how do you become cloud-based when you have invested so much in your legacy infrastructure? Take the necessary steps to leave it behind. Embrace the idea of creating an altogether new banking model, a digital banking model, which we might call “NewBank” (as opposed to “OldBank”).

The concept is a simple one. Instead of trying to take OldBank to the cloud—an environment that operates under a very different set of processes and procedures—build a NewBank model, born in the cloud. Run the two in parallel while you transfer data and applications from OldBank legacy systems to NewBank.

There are four, key benefits to this approach:

- Digital transformation starts now. You start creating new applications and moving data from old ones.

- Current business operations are uninterrupted. Operations of OldBank can be continuous and phased-out over time.

- The risk of transformation failure is mitigated. NewBank can be built in phases through customer-centric design principles and agile, “fail fast” development.

- A digital operating model becomes entrenched. You end up with a cloud-based operating model instead of a legacy, on-premises operating model with secondary cloud capabilities. With digital tools you can begin to address digital problems.

The cloud imperative

A digital operating model with the cloud at its center can include both private and public capabilities. There are also hybrid capabilities, based on both on-premises and cloud infrastructure. But it is fundamentally cloud-based. This is precisely where most banks are faltering; their core capabilities based on legacy infrastructure are beginning to collapse under the weight of aging technology, expensive maintenance, and costly upgrades.

Many banks today define their digital platform as an omnichannel interface that appears to keep customers happy but leaves their current operating model and systems unchanged. The argument goes something like this: “Let’s keep customers happy first—fixing the back office is too difficult. We’ll get to it one day.” But that day rarely comes. Even if it does, all the bank achieves is some degree of modernization, not the transformation it ultimately needs.