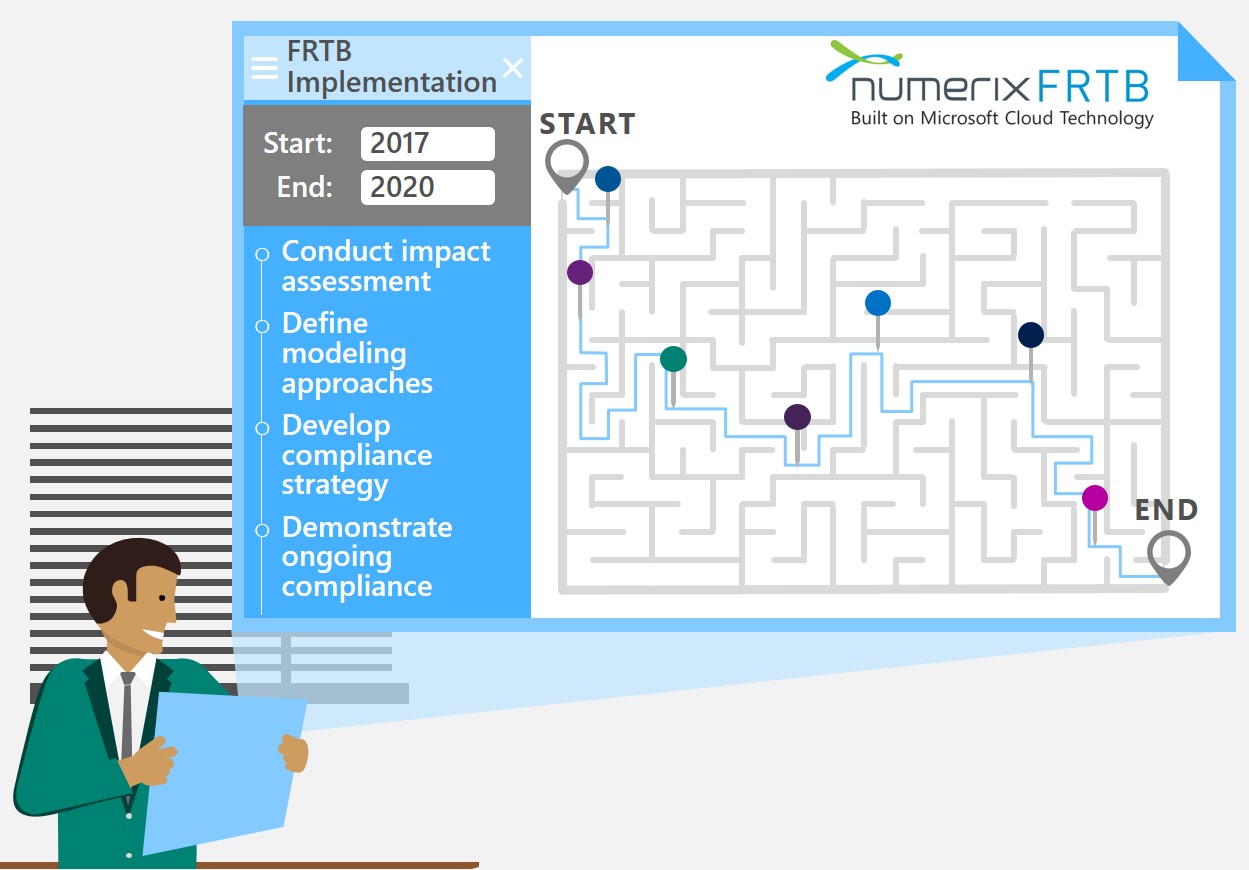

The FRTB Path to Readiness: Navigating a Maze of Obstacles

As the implementation deadline for Fundamental Review of the Trading Book (FRTB) nears, lack of clarity is causing the readiness path to seem like a hedge maze.

It’s been almost 18 months since the Basel Committee on Banking Supervision (BCBS) published FRTB regulations, and banks are realizing the path to compliance is more like a maze laden with grueling obstacles. Failure to comply by the deadline is not an option, so banks need to take action now. Success requires navigating around numerous obstacles such as unclear regulatory guidance, increases in overall capital requirements, stricter tests for internal model approvals, and a tight timeline. Compounding these difficulties are the technological challenges banks face, including inflexible legacy technologies unable to adapt to FRTB’s new modeling requirements, the need for enhanced data quality and aggregation capabilities, and computationally-burdensome risk metrics. Let’s examine some of these decision points to gain an understanding of what banks are up against as the implementation deadline nears.

Lack of technical clarification leaves many unanswered questions

Capital markets practitioners are critical of elements of the BCBS’ FRTB guidance due to its conflicting nature. One example is the profit and loss (P&L) attribution testing, which will impact whether banks are approved to use an internal model approach (IMA) for calculating market risk capital requirements for trading desks. The BCBS framework sets forth two possible testing methods but has not clarified which approach is the “official” approach, even after releasing a FAQ document in early 2017 that was supposed to provide answers. As a result, banks are unsure how to proceed. Some banks are expending resources preparing for both testing methods, or delaying all work in this area – neither of which is ideal.

Likewise, concerns are surfacing around how to deal with market illiquidity, which affects capital charges for Non-Modellable Risk Factors (NMRFs) under the IMA approach. Banks in regional markets will be especially affected, as many products – even long-dated government bonds – may not trade frequently in those markets for long stretches of time. The products will therefore be characterized as illiquid risk factors under FRTB, and they will attract punitive risk charges under the NMRF framework. This could impact liquidity even further, causing many banks to stop trading those products.

There is also a lack of clarity around whether all global regulators will be approaching FRTB in the same way, at the same rate. A disjointed global roll-out of FRTB could lead to hardships for banks with a global presence who are disadvantaged in some jurisdictions. In the spirit of looking out for number one, banks are focusing implementation efforts on areas of their businesses that are most likely to positively impact the bottom line – and putting off comprehensive compliance at their peril.[1]

FRTB technology is a big hurdle

Whether focusing on requirements needed for IMA approval, or simply trying to comply with the regulator-prescribed sensitivity-based approach, some banks are spending tens of millions of dollars in technology upgrades. Most must assess whether their existing software and analytics systems will have the computational power to support FRTB-compliant internal models, and the flexibility to adapt to the new modeling approaches. Other banks have brittle and rigid legacy systems in place that cannot scale with the demands of FRTB, and must apply a new solution no matter what.

Regardless of banks’ current infrastructure, the systems they move forward with must be able to reconcile front and middle office pricing models. Data and compute environments must be brought together to integrate, store, and validate massive amounts of data. To accurately run the approximately 8.7 billion simulations required per trading desk, banks must either totally overhaul their approach or buy brand new.[2]

The uncertainties surrounding FRTB make deciding on a technology approach even harder. Unfortunately, banks are running out of time to make these decisions and become adequately prepared for the FRTB deadline.

2017 is a crucial year for technology decisions

The Basel framework laying out FRTB regulations was finalized in 2016, leaving banks four years to make structural changes before they must begin reporting under FRTB in 2020. When factoring in implementation time, the latest a bank should begin the accreditation process is the beginning of 2019. Before initiating the accreditation process, banks need to test and apply their FRTB-compliant technology throughout 2018. Therefore, technology decisions must be made in 2017.

Making critical decisions when surrounded by uncertainty and pressed for time is strenuous. Even banks that are eager to become FRTB-ready are finding the technology solutions available to the market are unequipped to meet the full scope of their needs.

Numerix understands these obstacles and is uniquely positioned to help banks accelerate their FRTB readiness

Numerix FRTB, built on Microsoft Cloud technology, is the first FRTB solution available. As an industry leader in derivative pricing models and risk technology, Numerix is uniquely positioned to ease the pressures banks face. Numerix’s solution enables banks to start preparing for FRTB now with an early stage impact assessment to understand exactly how FRTB will affect their regulatory capital requirements and technology needs going forward. The results of these impact assessments provide clarity around the optimal modeling approach for financial institutions’ operations, empowering the development of cohesive compliance strategies.

Numerix FRTB also enables banks to easily demonstrate compliance on an ongoing basis. The solution’s high-performance, cloud-based risk engine provides the computational power needed to calculate the tremendous volume of daily simulations FRTB requires while delivering more efficient use of capital, improved levels of executive visibility into present and future needs, and greater confidence engaging with regulators.

To learn more about how Numerix FRTB provides regulatory reassurance, delivers capable compliance, and empowers banks to navigate the maze of FRTB, explore the app on Microsoft AppSource.

[1] http://www.numerix.com/risk-magazine-april-2017-special-report-fundamental-review-trading-book

[2] http://www.numerix.com/impact-report-xva-and-risk-transformation-establishing-data-fundamentals