Harnessing Customer Data Will Save Retail Banking

For decades, opening a new checking or savings account meant walking into a bank branch and talking to a teller. Home loans worked much the same way, and credit cards could only be received through an established bank or financial services company.

Since the early 2000s, however, retail banking services have become increasingly commoditized. New companies arose online, with no physical branches, to challenge established players and increase the amount of choice consumers have for their banking needs.

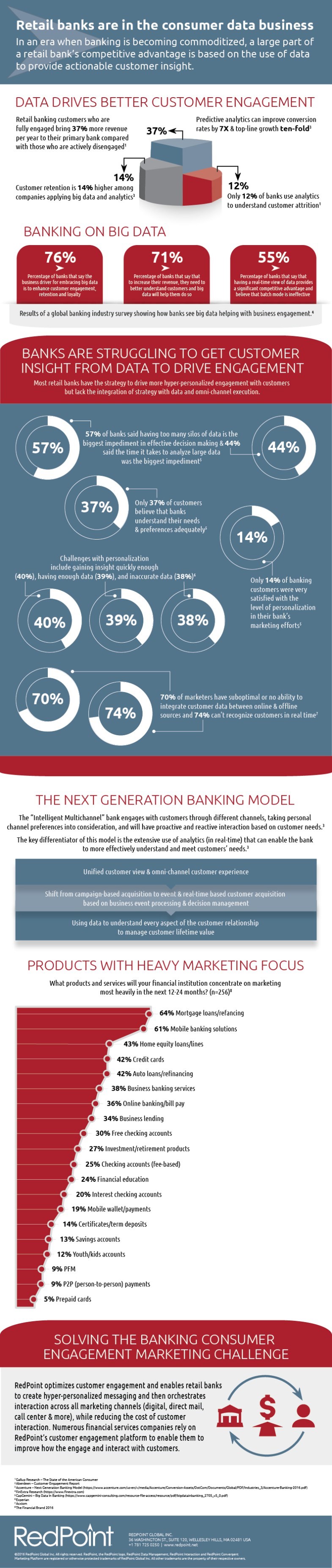

This presents a problem for retail banks, which must use their customer data to drive improved engagement through actionable customer insight. The results from using customer data this way are striking, as illustrated in RedPoint’s new infographic below:

Fully engaged retail banking customers bring in 37 percent more revenue per year to their primary bank versus customers that are actively disengaged. This makes customer engagement exceptionally profitable, so it’s good news that big data has gained the necessary cache among retail bankers. In fact, a recent Finextra report showed that banks understand how embracing big data can change how well they engage customers, with 76 percent of bankers saying customer engagement, retention, and loyalty are the business driver for adoption, and with 71 percent noting that big data will help them better understand customers and drive improved revenue. Using big data effectively can directly contribute to the bottom line: A recent report from PwC indicates that 90 percent of customers trust recommendations posted on social media websites and 71 percent are more likely to make a purchase based upon social media referral.

But time is short in the quest to harness and leverage customer data. The modern empowered consumer is unlikely to wait long for their bank to get their customer-centric act together. Recent Capgemini research showed that only 14 percent of customers were satisfied with the level of personalization in their bank’s marketing efforts. This is hugely disappointing, and indicates that banks have a long way to go toward fully understanding their customer.

Given the increasing fragmentation in the marketplace, with mobile, digital-first, and alternative payment solutions fast hitting the streets, retail banks can ill afford to not ramp up their use of customer data. This creates a new paradigm for retail bankers, who must engage customers through the channel of their choice and craft intelligent multichannel campaigns that include hyper-personalized offers and experiences.

This will likely involve an internal shift as well toward a culture more focused on creating value in customer interactions and involving predictive analytics to determine the next best action and drive deeper insight into the consumer’s needs and wants. Retail banks that can make this change effectively are more likely to thrive in the new, commoditized banking environment.

Many experts believe that the large global and national banks will have a major advantage in the movement to improve retail banking because they have the resources to invest in becoming more customer data driven. However, local and regional banks have a built-in advantage in their ability to provide a more personal touch, and blending a better digital experience with a satisfying offline experience is a powerful combination. Regardless of size, banks need to invest in new technologies that enable a more customer-centric approach. The good news is that, compared to the potential payoff, these technologies will not break the bank.

RedPoint Global helps enterprises to optimize customer engagement and deliver on their brand promise. RedPoint is a customer data solution hosted on the Microsoft Azure cloud platform, which enables organizations to unify their data and create an integrated view of customers, generate next best actions with automated analytics, and orchestrate the customer experience across touch points, data sources, and channels. Microsoft Azure’s Platform-as-a-Service and Infrastructure-as-a-Service offerings dramatically reduce time to deployment. Azure provides the agility and scalability needed to make changes to the environment as new requirements arrive, minimizing additional costs.

Read more on the Microsoft Banking & Capital Markets and Insurance blogs.